New vehicle supply is facing further “headwinds”, despite healthy order banks ahead of the March plate change, says Cox Automotive.

It believes the automotive sector could be heading towards continuing rapid changing market dynamics, similar to 2021, due to global political events.

Philip Nothard, insight and strategy director at Cox Automotive, said despite the rapidly changing global political situation, there are reasons to be optimistic, with healthy order banks for March registrations, albeit for specific manufacturers and particular models.

This could create an imbalance of profile of part-exchanges and future used vehicles entering the parc, however. The hope for Cox Automotive is that March will generate some “much-needed” used vehicles for the wholesale and remarketing sector and dealers.

According to Nothard, reports imply manufacturers are operating a 'sold order only' process or deciding to prioritise the retail channel, in addition to either limiting supply or offering no response to when production will resume.

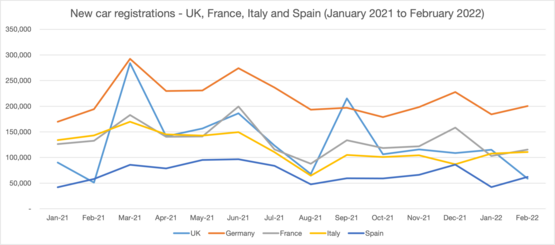

According to data from the Society of Motor Manufacturers and Traders (SMMT), 58,994 new cars were sold in the UK, an increase of 13.04% on the results from February 2021 – but still far off the pre-pandemic month performance of February 2020, where sales were 34.93% higher.

Cox Automotive published figures in the new edition of Autofocus, which represented Q1 2022 new car sales forecasts, giving best, mid, and worst-case scenarios. With the mid-case scenario looking to be the most likely, this result was close to the actual figures published by the SMMT, with a prediction of 56,256 new cars sold – representing a 4.6% difference on the actual statistics.

Nothard added: “With signs of a recovery in motion and with March 2022 seeing the release of the new ’22 registration, we’re optimistic to see a better March new car plate change month than the previous two years.

“Our mid-case scenario for the month will see around 330,645 new registrations. At the moment, the SMMT has recorded 174,081 new registrations over January and February, so I will be hoping to see around 332,723 registrations in March to reach even the mid-case scenario expected results. However, the situation in Eastern Europe could change the fortunes of the industry on its head once again.”

In the used market, February’s wholesale key indicators continued to display signs of a stable market created by the ongoing imbalance between supply and demand, which has existed since the summer of 2020.

Manheim lanes last month experienced three key indicator increases. This was seen in the average first-time conversion, which increased by 0.74% to 84.40% month-on-month. In addition, the average age of cars sold also slightly increased by 1.2% to 102.1 months, and the average mileage of cars sold increased by 396 miles to 70,558 miles.

Despite three key indicators experiencing month-on-month increases, used car values fell slightly, with the average sale price decreasing by 2.32% or £187, to £7,866. CAP Clean values also experienced a marginal month-on-month fall of 0.22%, to 98.04%.

Nothard said: “It’s increasingly likely that we will see a continuation of many of the market dynamics we saw in 2021. However, although there are signs of new vehicle supply returning, it is currently very dependent on those manufacturers who have managed to secure the necessary materials to build vehicles and therefore keep production lines running. And even then, those manufacturers can only fulfil quotas on select models and derivatives.

“While manufacturers are slowly getting to grips with their production issues, and the situation will improve as the year progresses, this will be a prolonged and gradual process. As a result, we will not see a flood of stock enter the market, but rather a gradual increase as the backlog of orders for new vehicles gets cleared, in turn generating much needed stock for the used market.”

More articles on:

Fleet News looks in detail at how you can start the journey to van electrification and speaks to those already well advanced in their transition about the innovative ways they overcome some of the problems.

Fleet News looks in detail at how you can start the journey to van electrification and speaks to those already well advanced in their transition about the innovative ways they overcome some of the problems.

We also bust myths about batteries and look at the technologies poised to come to market promising greater range and faster charging.

Openreach head of sustainability Abby Chicken explains how the UK's largest commercial fleet is managing the transition to electric, and we also look at 10 of the best electric car and van models due to come to market this year.

Enjoy the read

Steve Briers

Group editor

Fleet News

Read now

Matt has been an automotive journalist for nine years and has driven just about every new car and van that's on sale. As content editor - vehicles he is responsible for the automotive content on Fleet News and also contributes to Automotive Management. Prior to this, Matt worked in the automotive industry for 10 years.

Login to comment

Comments

No comments have been made yet.