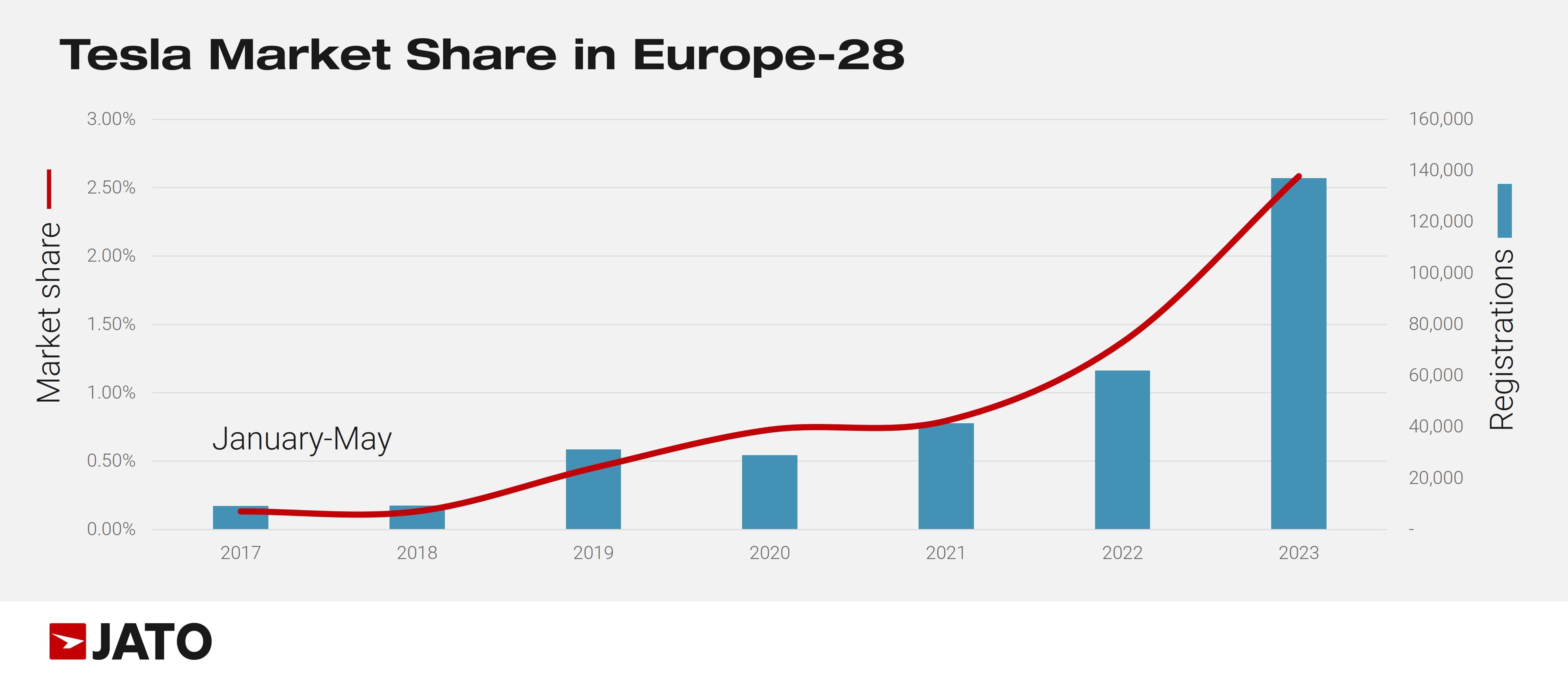

Tesla was the best performing manufacturer in Europe in May, winning 2.63% of the market, according to new sales data from Jato Dynamics.

In the same month last year, the US manufacturer’s market share was just 0.15%, however this was due to supply issues which caused registrations to drop.

Last month, Tesla registered close to 29,400 units, significantly higher than the monthly total seen in May 2021 (8,810 units), May 2020 (2,757 units), and May 2019 (4,087 units).

Felipe Munoz, global analyst at Jato Dynamics, said: “By making use of incentives and good market position, Tesla has been able to outperform its rivals, while part of the brand’s success is also explained by continuous price cuts.”

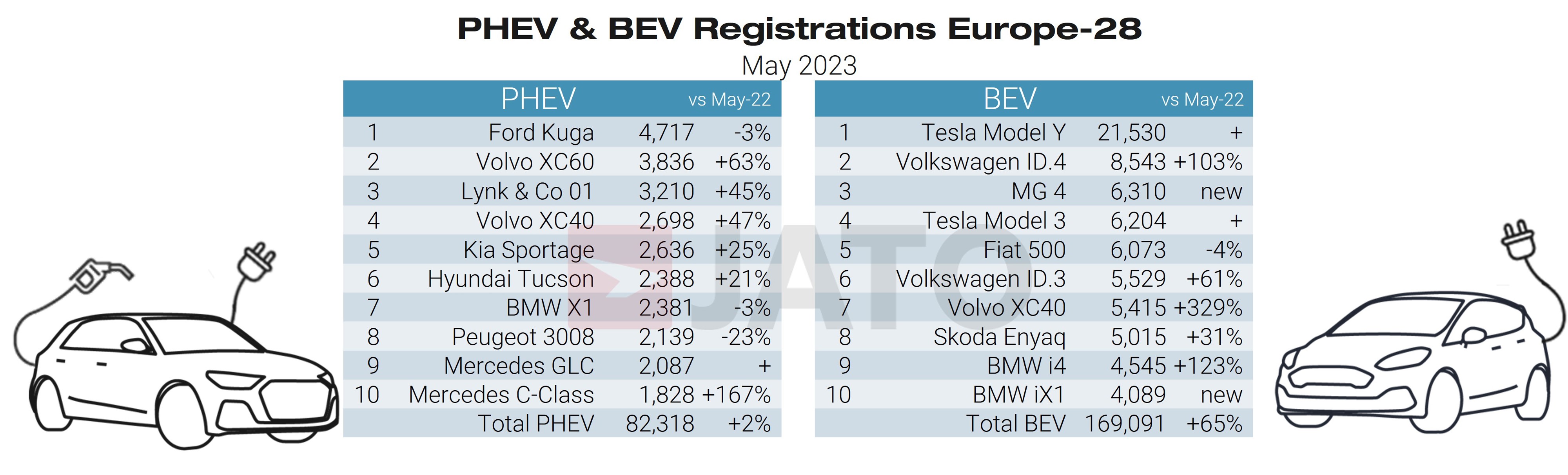

In the BEV segment, Tesla’s market share totalled 17.4% and 18.9% year-to-date, up from 12.2% in the same period last year – the largest market share increase by a significant margin at 6.7 points. SAIC, the owner of MG and Maxus, followed with an increase of 2.8 points, and in third place Volkswagen Group secured a market share increase of 2.7 points.

In contrast, Hyundai-Kia lost 5.6 points of share through May, followed by Stellantis, down by 3.4 points.

Total BEV registrations increased by 65% in May to 169,091 units accounting for 15% of all new vehicle registrations during the month.

In addition to the success of the Model Y – Europe’s best-selling car between January and May – the market is also being shaken by the MG 4, which secured a record third position in the BEV ranking by model with 6,310 units, ahead of its rival the Volkswagen ID3 with 5,529 units.

The Volkswagen ID4 also performed well with 8,543 units (+103%) as the second most popular BEV of the month.

There were also strong increases for the Volvo XC40 BEV (+329%), BMW i4 (+123%), and the BMW iX1, all of which entered the top in the BEV ranking by model in May.

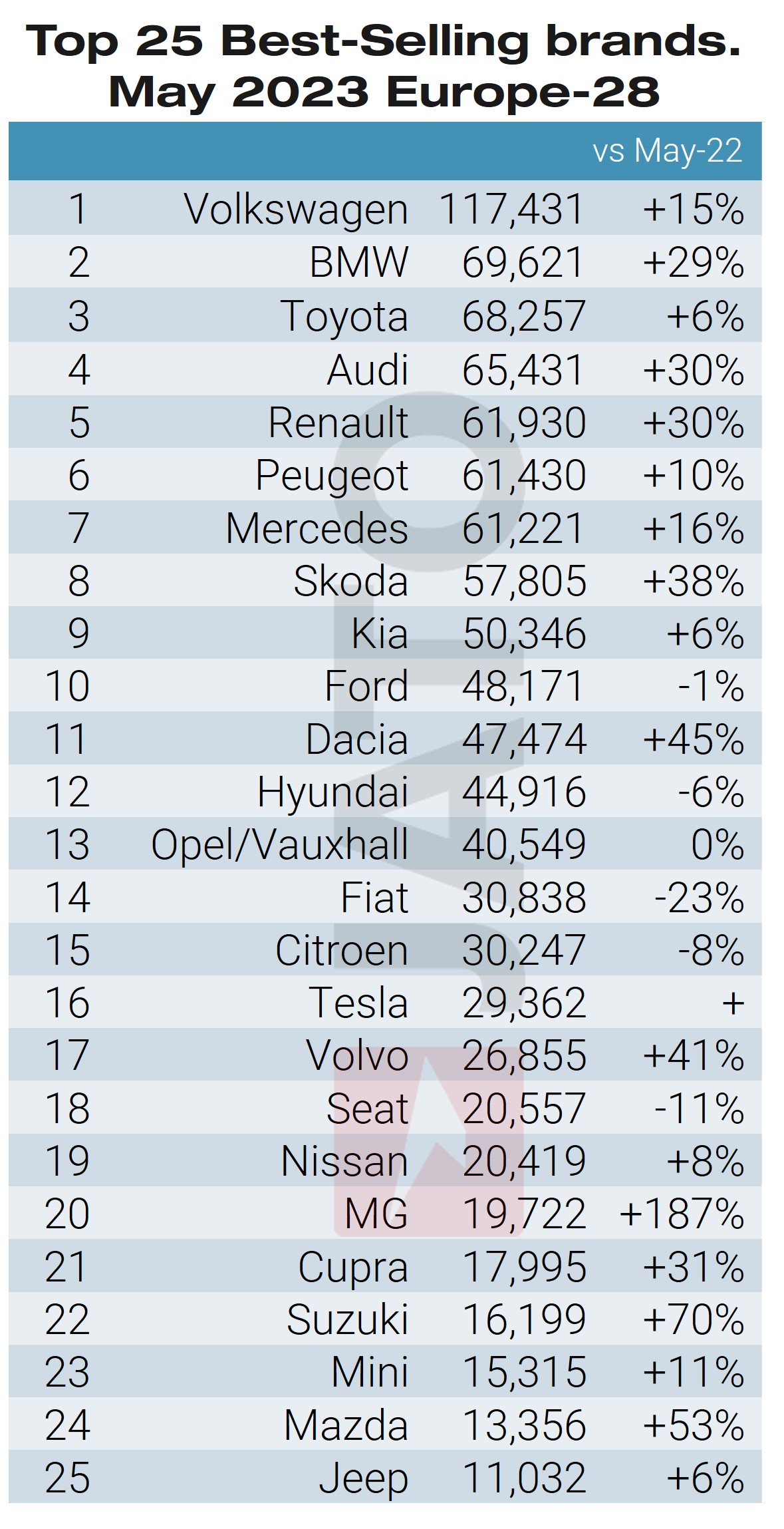

Looking at overall sales across 28 European countries, new vehicle registrations totalled 1,116,472 in May – an 18% increase on the 943,435 in the same month last year.

This takes the year-to-date total to 5.3 million units, up by 17%.

Munoz said: “While BEVs and SUVs continue to drive the recovery of the industry, growth across all segments has not been enough to bring total volume back to pre-pandemic levels.”

Total volume year-to-date fell short of the 6.93 million units registered in the same period in 2019, and was similar to the levels seen in 2021, when markets still recovering from lockdowns were hit by the semi-conductor shortage.

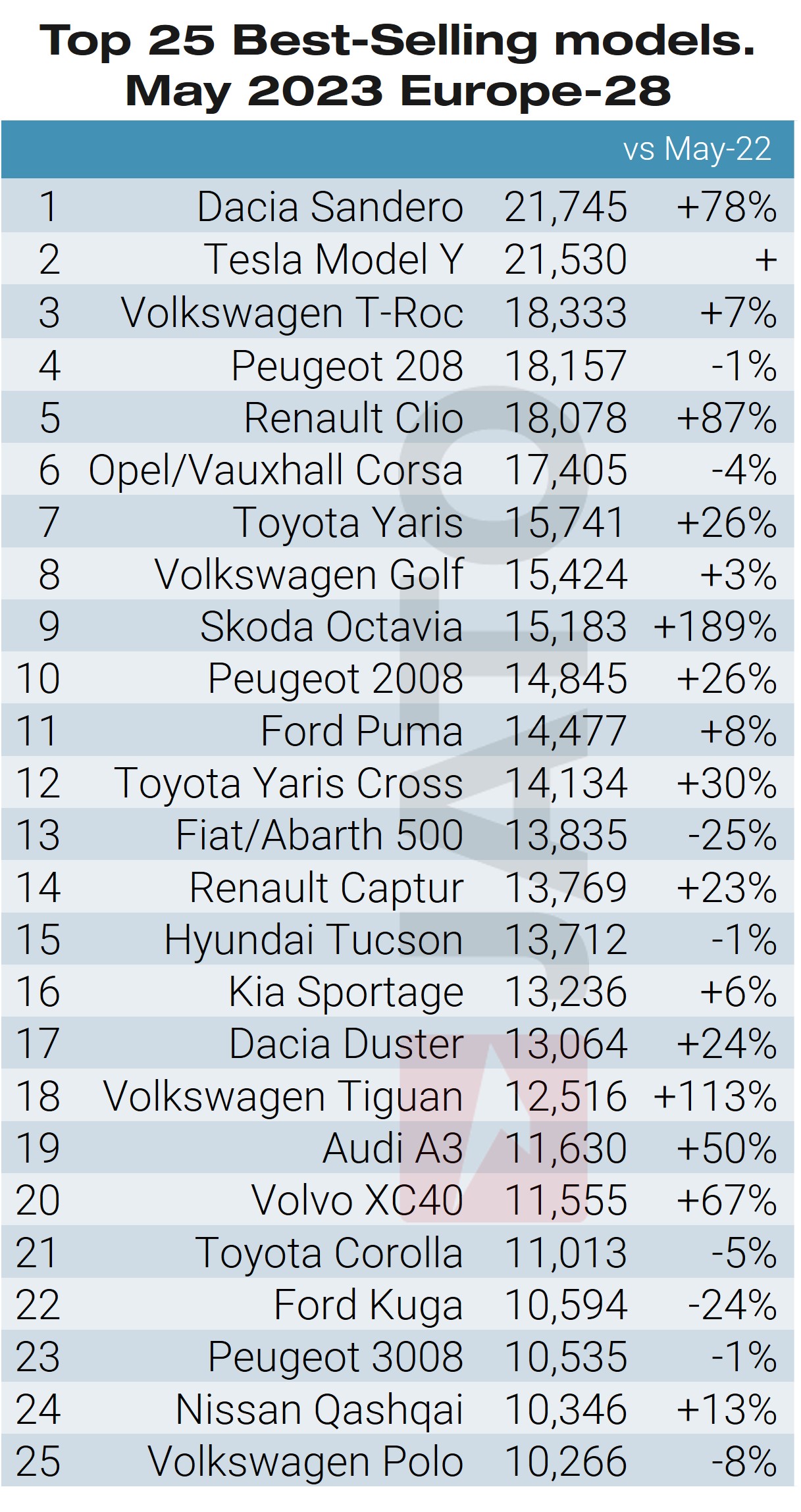

The Dacia Sandero leads again

The low-cost model from Dacia again secured the top spot in the overall ranking by model with more than 21,700 units – up by 78% with sales were boosted by strong increases in key markets included France, Italy, Spain, and Germany.

Munoz explained: “While the Model Y plays its role in the electric high-end EV segments, the Sandero has continues to gain traction in the low-end ICE segments.”

The Tesla Model Y followed in second place with 21,530 units, up by 1838% compared with May 2022.

Munoz, added: “The popularity of the Model Y has been confirmed in Europe, and it stands a good chance of leading both the European and global ranking model ranking by the end of the year.”

Among the latest launches, Renault registered 7,174 units of the Austral, becoming the brand’s fourth best-selling vehicle; Jeep registered 4,290 units of the Avenger, offsetting the drops posted by the Compass (-41%) and Renegade (-32%), to become its best-seller in May; Alfa Romeo registered 3,240 units of the Tonale, accounting for 69% of the brand’s total volume; and Peugeot registered 1,923 units of the 408.

More articles on:

Fleet News looks in detail at how you can start the journey to van electrification and speaks to those already well advanced in their transition about the innovative ways they overcome some of the problems.

Fleet News looks in detail at how you can start the journey to van electrification and speaks to those already well advanced in their transition about the innovative ways they overcome some of the problems.

We also bust myths about batteries and look at the technologies poised to come to market promising greater range and faster charging.

Openreach head of sustainability Abby Chicken explains how the UK's largest commercial fleet is managing the transition to electric, and we also look at 10 of the best electric car and van models due to come to market this year.

Enjoy the read

Steve Briers

Group editor

Fleet News

Read now

Gareth has more than 20 years’ experience as a journalist having started his career in local newspapers in the 1990s. Prior to joining Fleet News in 2008, he worked in the public sector as a media advisor and is currently news editor at Fleet News.

Login to comment

Comments

No comments have been made yet.